Did you know that MyPay has been making waves in the digital arena as the new one-stop e-government services platform? We’ve been in the news quite a bit over the recent weeks.

If you have yet to start using MyPay or are still wondering whether to use the platform or not, take a look at what has been said in the media. It may help you make up your mind.

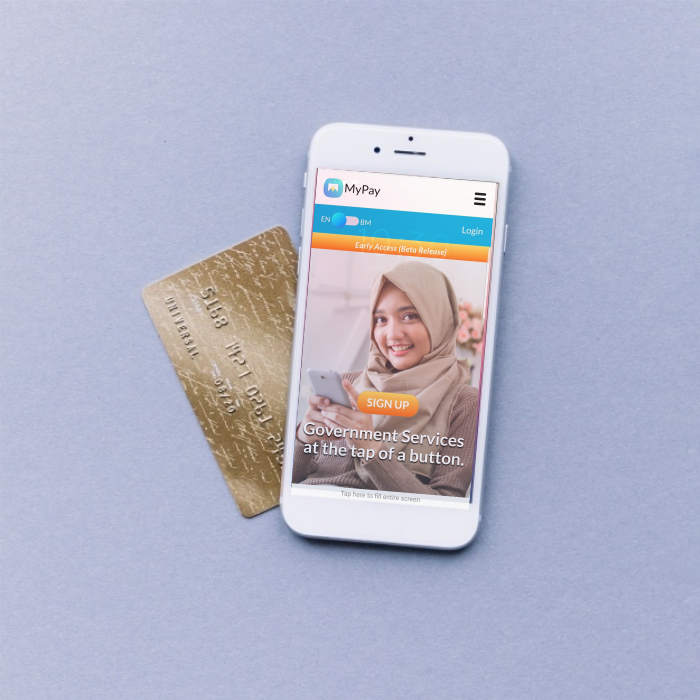

What is MyPay?

Malay Mail describes MyPay as a platform that accesses various public services, allowing its users to easily make payments online. It aims to offer a one-stop platform for all queries and payments related to Government agencies.

Funnily enough, MyPay can easily be mistaken as yet another e-wallet to hit the market! However, Digital News Asia and The Adventures of Vesper confirmed with its founders that it is nothing of the sort. It doesn’t work like a typical e-wallet where you are to deposit money before making any online payments. It simply allows you to pay all your government-related bills using your credit card or via online banking.

Quoted as “One Platform To Rule Them All” by the Vulcan Post, MyPay currently has 17 agencies on its platform including Royal Malaysia Police (PDRM), Kuala Lumpur City Hall (DBKL), National Higher Education Fund Corporation (PTPTN) and more planned in the near future.

A brief history of MyPay

The company behind MyPay is none other than Dapat Vista (M) Sdn Bhd, the same company that has been providing the government SMS services for the past 14 years.

Kiranjit Kaur from Digital News Asia in her BFM tech talk programme, quoted that Dapat was able to develop MyPay within eight months thanks to existing data connectivity and close working relationship with the Government – it would have been difficult if they were merely a typical start-up.

What about competition?

You might be wondering why you should use MyPay instead of, MyEG for example. Interestingly, MyPay’s co-founder and chief executive officer, Nick Liew, is confident that MyPay is more user-friendly and offers more services. Read more about this via The Star

MyPay's CEO, Nick Liew

Although MyPay is not in direct competition with any of its peers in digital payments, some form of competition is good for the users. It not only offers alternative payment avenues, but also encourages service providers to continue improving on their services in general.

What else was said?

As queried by Vulcan Post, security can be an issue here since one needs only a person’s IC number for various info retrieval. As an added precaution, MyPay has implemented a facial recognition feature (e-Know Your Customer or eKYC) that requires users to submit a picture of their IC and a selfie shot during the registration process.

Raja Idris, the writer from Pokde.net, felt that MyPay is really a one-stop platform that’s on hand for users at any time.

Best of all, MyPay is free to use! You only have to pay a service charge of RM0.50 - RM1 for every transaction made when making payments for loans, bills, or summons.

But, if you’re just there to check on your information such as your outstanding summons or your outstanding PTPTN loan amount, rest assured that it won’t cost you a single cent.

If you want to experience how MyPay works, please click here.